Investment Management

Macro Value Monitor

The Initial Education from a Secular Pivot

October 5, 2023

Despite the Federal Reserve raising interest rates to a 22-year high, the economy remains surprisingly resilient, with estimates putting third-quarter growth on pace to easily exceed its 2% trend. It is one of the factors leading some economists to question whether rates will ever return to the lower levels that prevailed before 2020 even if inflation returns to the Fed’s 2% target over the next few years…

~ The Wall Street Journal, August 20, 2023

Change of a long term or secular nature is usually gradual enough that it is obscured by the noise caused by short-term volatility. By the time secular trends are even acknowledged by the majority, they are generally obvious and mature.

In the early stages of a new secular paradigm, most are conditioned to hear only the short-term noise they have been conditioned to respond to by the prior existing secular condition. Moreover, in a shift of secular or long-term significance, the markets will be adapting to a new set of rules, while most market participants will still be playing by the old rules…

~ Bob Farrell, Merrill Lynch

One and three hundred years before the enormity of the present dilemma began to dawn on the Federal Reserve, a similar moment arrived within the stone walls of the Banque Royale. You may recall the scene we visited last year.

By the end of 1719, property prices in Paris had risen so much that even wealthy Parisians were having difficulty affording a home. A clamoring for real estate over the prior year had driven prices so high that the rental yield on properties in the city had fallen to just 2%. This not only made owning real estate as an investment unprofitable, it also made buying a home to live in prohibitively expensive. Yet amid those hostile market conditions, few of the Parisian elite felt like there was any alternative except to try to buy something, anything, before prices rose further, even if it was in one of the less desirable neighborhoods across the Seine on the left bank.

For everyone else in the city, the daily cost of living was spiraling higher as well. In order to buy meat in the market, or simply a loaf of bread, it seemed as if more and more livre notes were needed each week. And it was not only eating that was becoming more expensive. As property prices spiraled higher in the city, rents began rising as well, and even keeping one’s home heated was becoming difficult; the price of wood had climbed higher than in anyone’s memory.

Outside Paris, prices were also changing rapidly. Landowners in the countryside found themselves suddenly wealthier in 1719, as a flood of Parisians fleeing the prohibitive costs of the city created bidding wars for land in the country. Yet cheap land had grown scarce, and the increasing price of quality farmland quickly percolated down to drive up the cost of commodities of all sorts, including the price of grain used to feed the animals that transported food to Paris. Eventually, even newly wealthier landowning farmers found themselves earning less, as the cost of producing and selling their goods rose faster than they could increase their own prices at the market.

While few seemed to understand why prices were rising so much, the upheaval seemed to be emanating from the growing commotion taking place every day on rue Quincampoix.

Earlier that year, a market had sprung up on a short, narrow street set back from the Seine in the 1st arrondissement, on the right bank. It was a curious place for such a frenzied scene, as the street was only 30 feet wide in the narrows between the four and five story buildings on either side. A cart had barely enough room to pass through amid the throngs of onlookers. And yet, day in and day out, crowds assembled first thing in the morning in the narrow lane to begin trading the hottest commodity of all in 1719: Company of the West shares.

In fact, despite its cramped confines, the location of the impromptu market on rue Quincampoix was no accident: it had sprung up right outside the front door of the Banque Royale.

The Banque Royale and the Mississippi Company, as the Company of the West was commonly known, were both directed by John Law, and the astounding 20-fold growth in the price of Mississippi Company shares in 1719 had unfolded hand-in-hand with the 20-fold increase in notes emitted by the Banque Royale. As astute traders on rue Quincampoix knew all too well, every change in the supply of banknotes proved to be the driving factor behind subsequent changes in the price of Mississippi Company shares. Those who were privy to first knowledge of any new actions by the Banque Royale were positioned to profit from the subsequent reaction in the shares, and the place to gain that edge was to remain camped right outside the Banque Royale’s front door on rue Quincampoix.

The scene on rue Quincampoix outside the Banque Royale in Paris

Yet as the price of Mississippi Company shares soared to 10,000 livres in December 1719 from 550 livres in May, the vast expansion of the money supply that propelled the shares had begun to spread beyond trading on rue Quincampoix. Property prices began to soar as the newly-wealthy owners of Mississippi Company shares traded them for luxurious homes in the city, as well as large estates in the countryside. Money also began flowing out into the broader economy, as shareholders sold shares, or borrowed against their value, to spend lavishly.

As prices began to rise for everything from land to wheat to fine imports from the Spanish Netherlands in late 1719, it marked a pivotal moment for the citizens of France: the arrival of inflation. It also marked the end of the Mississippi Bubble, and the beginning of the inflationary bust.

* * *

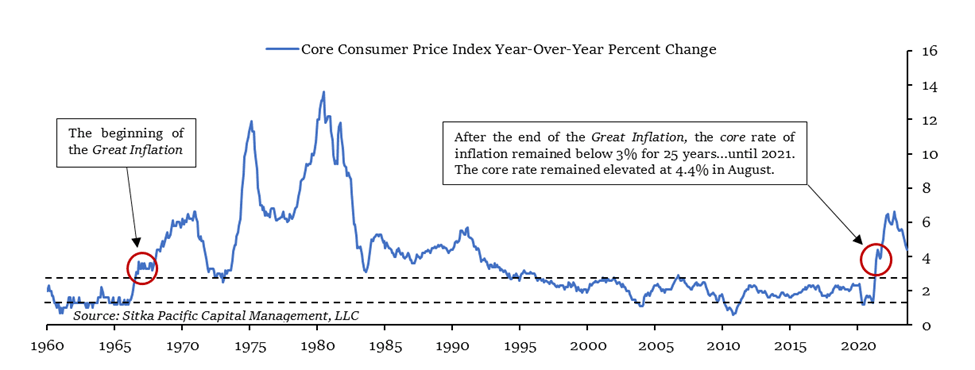

It has now been eighteen months since the Federal Reserve ended the massive quantitative easing program carried out in response to the Covid-19 pandemic, and given the long and variable lags with which changes in monetary policy affect prices, the early, first-order impact of that massive monetary expansion is only just now fading from the scene. The year-over-year change in the headline Consumer Price Index over the course of the past sixteen months reflects that: it has fallen from just below 9% to just above 3%, as commodity prices settled down after the dramatic increases in 2020 and 2021. The year-over-year rate of change in the core Consumer Price index, shown below, remains elevated over the range of the past 25 years, but has also fallen from its peak rate in 2022.

Yet there is far more to an inflation dynamic, once entrenched, than the early, first order reaction, as John Law eventually discovered. In late 1719, the first hint of trouble from beyond first-order reactions came when a small number of astute citizens no longer believed the proliferating notes of the Banque Royale were a trustworthy store of long-term value – and discretely sought an exit.

The closure of the Banque Royale on the last day of November 1719, along with the subsequent decrees which mandated use of its banknotes, were early signs that the market environment had pivoted away from the initial, exuberant expansion resulting from the massive growth of the money supply, and had begun to price in the full inflationary cost.

As prices soared for homes, land, and everyday goods, it shattered the underlying assumption that prices were mainly a function of supply, demand, and progress. People began to understand that prices could also change from an erosion in the value of the notes they held in their hand, and the closure of the Banque Royale in November 1719 resulted from a few of those people demanding to exchange their paper banknotes for something of trustworthy value – gold and silver coin.

The erosion of trust in the value of a currency is one of the main second-order impacts of large monetary expansions. Once that trust is lost, it is difficult, and sometimes impossible, to get back.

John Law found out in 1720 that restoring that trust ultimately involved sacrificing his entire scheme to bring prosperity to France, and relieve the Royal Treasury of its debts, by expanding the money supply. In the end, once the French citizenry lost faith that their banknotes would hold value, the stampede out of banknotes – and out of assets denominated in those banknotes – began. The prices of things which had previously only gone up – homes in Paris, land in the countryside, and especially Company of the West shares – suddenly found few bidders at any banknote-denominated price. The rush into gold and silver in 1720 ultimately restored the balance between the value of real assets and productive assets that had existed prior to 1719, and by 1721, rue Quincampoix was again a sleepy backstreet.

* * *

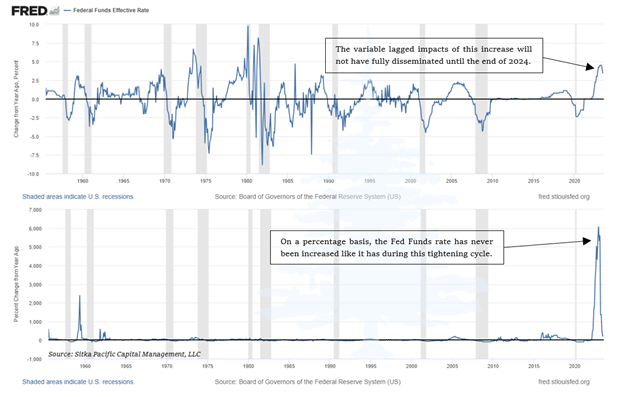

Since last year, the Federal Reserve has been attempting to achieve what John Law failed to do: restore faith in the value of the dollar before a second-order response— an entrenched inflationary psychology – takes root. Over the past year and a half, the Fed Funds rate has been taken vertical in that effort, increased from 0%-0.25% to 5.25%-5.5%.

The charts above place the rise in the Fed Funds rate over the past year and a half into perspective. This has been one of the largest increases in the Fed Funds rate in the post-war era; only the tightening campaigns in 1973-74 and the early 1980s witnessed sharper rate increases. As is shown in the bottom panel, on a percentage basis, i.e. scaled against the interest rate at the beginning of the rate hike campaign, the current cycle has produced the largest percentage increase ever.

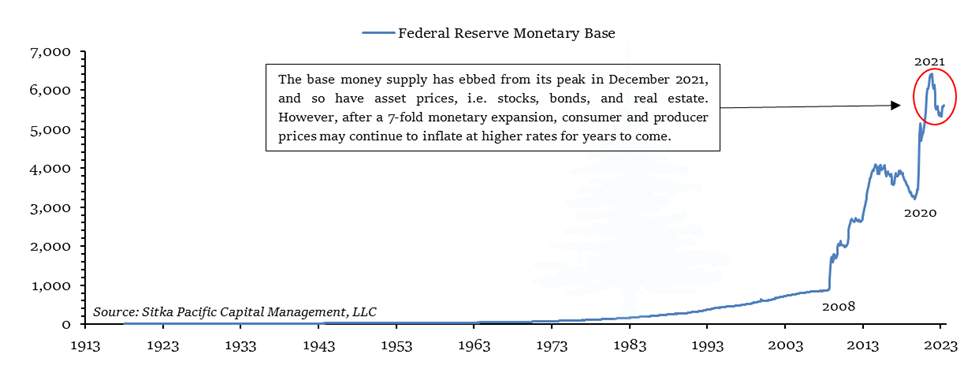

At the same time as it has increased interest rates, the Federal Reserve has been doing what Law fatefully attempted to do at the Banque Royale in May 1720: shrink its balance sheet. After reaching its high-water mark at $8.965 trillion in April of last year, the Fed has disposed of $941 billion in assets, leaving its balance sheet at $8.024 trillion as of September 20th. This has had a predictable impact on the base money supply over the past year, highlighted below, and also in broader measures such as M2.

Early last year we reviewed the first and second time the Federal Reserve shrank its balance sheet, in the early 1920s and the mid-1930s. Those episodes highlighted an important point as the Federal Reserve embarked on quantitative tightening: there was little difference between the reaction of people and prices in 1720 versus the reactions of people and prices to early modern attempts to shrink the money supply. And over the past year, we have witnessed yet another demonstration of the impact of quantitative tightening, as stocks, bonds, commodities, and real estate have all felt the weight imparted by a shrinking money supply. Bank failures, like we saw earlier this year, have been a regular feature of broad declines in money supply historically.

Yet, at the same time, while consumer prices and asset prices have clearly felt the impact of the restrictive pivot in monetary policy over the past two years, the evidence has been growing that these first-order reactions may just be the initial response to a much larger secular pivot.

In his speech at this year’s annual conference of monetary policymakers in Jackson Hole, Wyoming, Fed Chair Jerome Powell highlighted this growing body of evidence that the economy is now being governed by a different set of inflationary forces.

He began by recounting a selective history of how inflation arose over the past few years, notably leaving out any mention of the increase in the money supply in the decade prior to 2020, or the massively expansionary policies of the Federal Reserve in 2020 and 2021. Instead, he framed the emergence of inflation as an almost happenstance meeting of pandemic and war:

The ongoing episode of high inflation initially emerged from a collision between very strong demand and pandemic-constrained supply. By the time the Federal Open Market Committee raised the policy rate in March 2022, it was clear that bringing down inflation would depend on both the unwinding of the unprecedented pandemic-related demand and supply distortions and on our tightening of monetary policy, which would slow the growth of aggregate demand, allowing supply time to catch up. While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.

On a 12-month basis, U.S. total, or “headline,” PCE (personal consumption expenditures) inflation peaked at 7 percent in June 2022 and declined to 3.3 percent as of July, following a trajectory roughly in line with global trends. The effects of Russia’s war against Ukraine have been a primary driver of the changes in headline inflation around the world since early 2022. Headline inflation is what households and businesses experience most directly, so this decline is very good news. But food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed…

On a 12-month basis, core PCE inflation peaked at 5.4 percent in February 2022 and declined gradually to 4.3 percent in July. The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal. We can’t yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters. Twelve-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability.

Powell concluded his speech with the following:

Turning to the outlook, although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role. Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.

Restrictive monetary policy has tightened financial conditions, supporting the expectation of below-trend growth… But we are attentive to signs that the economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust. In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up. Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy.

For those of us who have been following the Federal Reserve for a long time, the account above summarizing the sources of inflation represents a disingenuous characterization, at best. Lest we forget, the strong demand that collided with pandemic-constrained supply appeared just after the sharpest decline in GDP since the 1930s, and was the direct result of trillions of dollars of monetary and fiscal stimulus that followed. Without that stimulus, which was underwritten by the Federal Reserve, and which continued all the way into early 2022, there would have been no inflationary collision from such strong demand.

Selective histories like the narrative above exclude the primary reason inflation has proven stickier than expected over the last two years, and they also fatefully misdirect investors’ expectations. It is a misdirection similar to late 1719, when investors in Paris continued to wonder why the prices of homes, land, and goods of all kinds were rising all around them, while behind the scenes John Law continued to expand the supply of banknotes by leaps and bounds into 1720. Inflation of the kind we are experiencing today, like the inflation citizens of France experienced in 1719 and 1720, is the end result of a large increase in the base supply of money upon which all credit stands.

As is clear in the above chart showing the monetary base, the decline since 2021 is small relative to the growth since 2008. Based on this alone, it has not been difficult to understand why inflation has proven to be more persistent, and less transient, than expected.

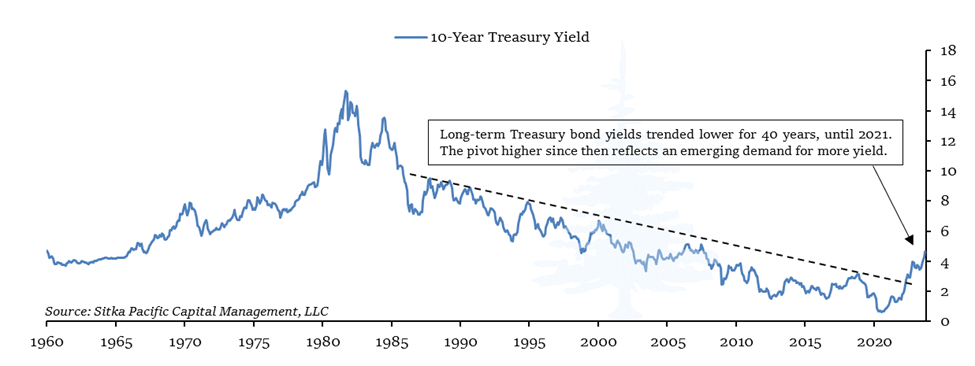

It was also not difficult to understand the risk embedded in long-term bonds when Treasury yields were hovering at 1-2% in 2021 amid inflation that had climbed above 5%. Great Mistakes of this magnitude have a tendency to erode confidence once prices begin rising, and it is this type of second-order impact that we may be witnessing in the bond market right now.

The pivot shown in the chart above represents a secular pivot into a new regime, one that has simultaneously brought an end to the Bountiful Triple Dip investors have enjoyed over the past four decades, and an end to the Federal government’s ability to rely on artificially low rates to hide the cost of the growing national debt. It has set in motion a new dynamic that has been easy to miss amid the constant noise in the markets, but which is unmistakable when looked at through the lens of financial history.

Through that lens, the chart above represents an example of investors “seeking an exit,” similar to how astute investors in late 1719 sought an exit from paper livres once they lost confidence that the banknotes would hold their value in the long run.

One of the unmistakable signs of eroding confidence is a demand for higher yields, and this past month the yield of the 10-year Treasury note climbed to 4.6%, which is the highest it has been in sixteen years. With the Federal Reserve no longer buying them, the market yield for bonds has been unshackled from the largest player in the market, and the rapid rise over the past year reflects an emerging demand for more yield in exchange for holding Treasuries.

It also may reflect an early second-order erosion of faith in the long-term value of the dollar. This past month, the Federal debt climbed above $33 trillion for the first time, which is an increase of $3 trillion from $30 trillion just three months ago in June. The national debt, including its rising annual cost from rising interest rates, is now growing at a faster rate than the real economy. This is an unsustainable dynamic that is not dissimilar to the Mississippi Company’s need to continuously sell shares to fund its spending, all the while depending on the Banque Royale to facilitate the shares sales by issuing more banknotes. Long before the unsustainable nature of this relationship became obvious to the average French person as things fell apart, rates and real assets had begun to rise as astute investors made their exit.

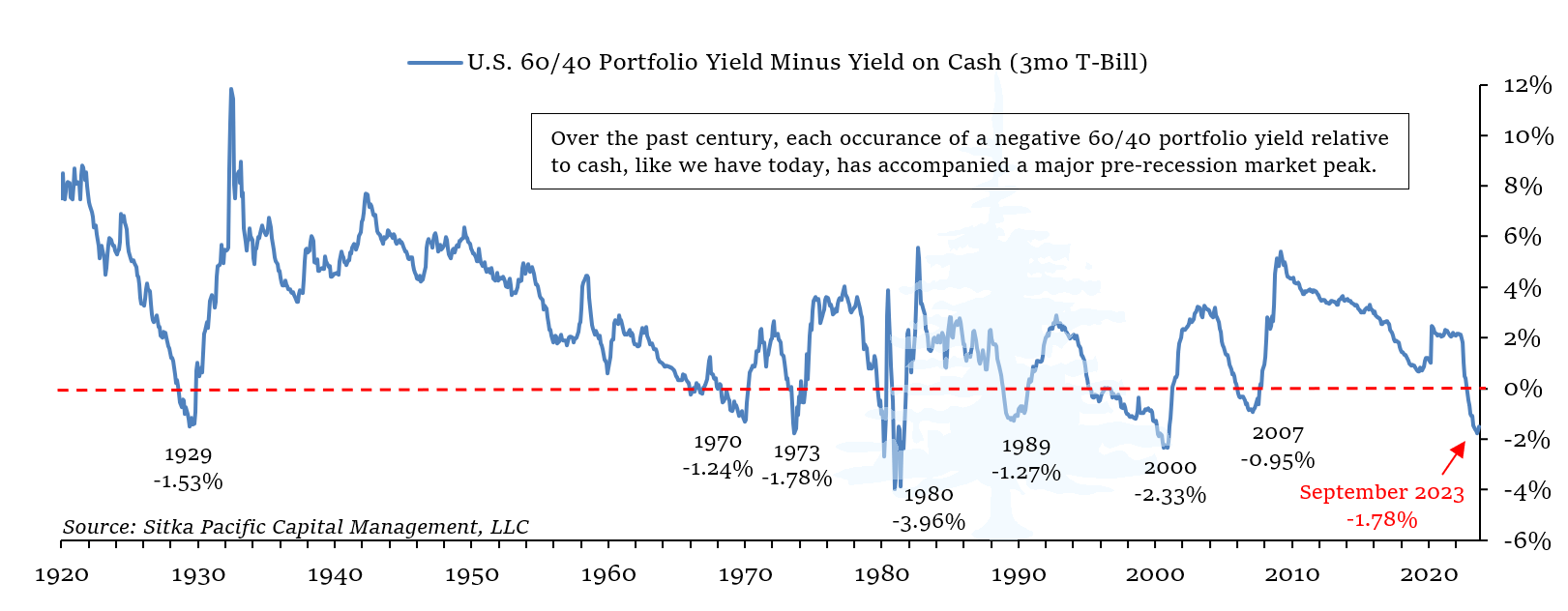

Yet while the yield on long-term bonds has risen over the past two years, it is clear that the vast majority of investors in U.S. stocks and bonds have not yet headed for the exit. The underlying yield of a standard 60/40 portfolio of stocks and bonds sank to 1.78% below the yield cash receives when invested in short-term T-Bills, and the yield differential between a portfolio of stocks and bonds since 1920 with cash is shown below. If you are familiar with market history, every prior instance of a negative portfolio yield relative to cash over the past century – in 1929, 1970, 1973, 1980, 1989, 2000, and 2007 – has marked a major pre-recession market peak.

The negative yield above represents a looming issue for investors. Although a standard 60/40 portfolio suffered its largest loss in half a century last year, the ongoing faith in stocks and bonds, represented by the lower portfolio yield relative to cash, is a sign that investors largely believe Chair Jerome Powell that the Federal Reserve will maintain its restrictive monetary policy until the deed is done, and inflation returns to its 2% target. In this benign outcome, interest rates would decline back to the 2%-3% range, leaving stocks and bonds well supported at current valuations.

Yet if history is any guide, we are instead on the cusp of an erosion of the confidence in that benign outcome, which will see the yield from stocks and bonds move higher from where they are today.

The losses in stocks and bonds in 2022 represented an initial education of the impact rising yields higher inflation have on portfolio value, and for many those losses came as a shock. Yet with the combined yield of stocks and bonds far below the yield on cash, the bulk of the education from the ultra-low yields in recent years may still lie ahead.

* * *

Return to Memos, Articles, & Letters

The content of this document is provided as general information and is for educational purposes only. It is not intended to provide investment or other advice. This material is not to be construed as a recommendation or solicitation to buy or sell any security, financial product, instrument or to participate in any particular trading strategy. Not all securities, products or services described are available in all countries, and nothing herein constitutes an offer or solicitation of any securities, products or services in any jurisdiction where their offer or sale is not qualified or exempt from registration or otherwise legally permissible.

Although the material herein is based upon information considered reliable and up-to-date, Sitka Pacific Publishing, LLC does not assure that this material is accurate, current, or complete, and it should not be relied upon as such. Content in this document may not be copied, reproduced, republished, or posted, in whole or in part, without prior written consent from Sitka Pacific Publishing, LLC — which is usually gladly given, as long as its use includes clear and proper attribution. Contact us for more information.

© Sitka Pacific Publishing, LLC

The Initial Education from a Secular Pivot

October 5, 2023

Despite the Federal Reserve raising interest rates to a 22-year high, the economy remains surprisingly resilient, with estimates putting third-quarter growth on pace to easily exceed its 2% trend. It is one of the factors leading some economists to question whether rates will ever return to the lower levels that prevailed before 2020 even if inflation returns to the Fed’s 2% target over the next few years…

~ The Wall Street Journal, August 20, 2023

Change of a long term or secular nature is usually gradual enough that it is obscured by the noise caused by short-term volatility. By the time secular trends are even acknowledged by the majority, they are generally obvious and mature.

In the early stages of a new secular paradigm, most are conditioned to hear only the short-term noise they have been conditioned to respond to by the prior existing secular condition. Moreover, in a shift of secular or long-term significance, the markets will be adapting to a new set of rules, while most market participants will still be playing by the old rules…

~ Bob Farrell, Merrill Lynch

One and three hundred years before the enormity of the present dilemma began to dawn on the Federal Reserve, a similar moment arrived within the stone walls of the Banque Royale. You may recall the scene we visited last year.

By the end of 1719, property prices in Paris had risen so much that even wealthy Parisians were having difficulty affording a home. A clamoring for real estate over the prior year had driven prices so high that the rental yield on properties in the city had fallen to just 2%. This not only made owning real estate as an investment unprofitable, it also made buying a home to live in prohibitively expensive. Yet amid those hostile market conditions, few of the Parisian elite felt like there was any alternative except to try to buy something, anything, before prices rose further, even if it was in one of the less desirable neighborhoods across the Seine on the left bank.

For everyone else in the city, the daily cost of living was spiraling higher as well. In order to buy meat in the market, or simply a loaf of bread, it seemed as if more and more livre notes were needed each week. And it was not only eating that was becoming more expensive. As property prices spiraled higher in the city, rents began rising as well, and even keeping one’s home heated was becoming difficult; the price of wood had climbed higher than in anyone’s memory.

Outside Paris, prices were also changing rapidly. Landowners in the countryside found themselves suddenly wealthier in 1719, as a flood of Parisians fleeing the prohibitive costs of the city created bidding wars for land in the country. Yet cheap land had grown scarce, and the increasing price of quality farmland quickly percolated down to drive up the cost of commodities of all sorts, including the price of grain used to feed the animals that transported food to Paris. Eventually, even newly wealthier landowning farmers found themselves earning less, as the cost of producing and selling their goods rose faster than they could increase their own prices at the market.

While few seemed to understand why prices were rising so much, the upheaval seemed to be emanating from the growing commotion taking place every day on rue Quincampoix.

Earlier that year, a market had sprung up on a short, narrow street set back from the Seine in the 1st arrondissement, on the right bank. It was a curious place for such a frenzied scene, as the street was only 30 feet wide in the narrows between the four and five story buildings on either side. A cart had barely enough room to pass through amid the throngs of onlookers. And yet, day in and day out, crowds assembled first thing in the morning in the narrow lane to begin trading the hottest commodity of all in 1719: Company of the West shares.

In fact, despite its cramped confines, the location of the impromptu market on rue Quincampoix was no accident: it had sprung up right outside the front door of the Banque Royale.

The Banque Royale and the Mississippi Company, as the Company of the West was commonly known, were both directed by John Law, and the astounding 20-fold growth in the price of Mississippi Company shares in 1719 had unfolded hand-in-hand with the 20-fold increase in notes emitted by the Banque Royale. As astute traders on rue Quincampoix knew all too well, every change in the supply of banknotes proved to be the driving factor behind subsequent changes in the price of Mississippi Company shares. Those who were privy to first knowledge of any new actions by the Banque Royale were positioned to profit from the subsequent reaction in the shares, and the place to gain that edge was to remain camped right outside the Banque Royale’s front door on rue Quincampoix.

The scene on rue Quincampoix outside the Banque Royale in Paris

Yet as the price of Mississippi Company shares soared to 10,000 livres in December 1719 from 550 livres in May, the vast expansion of the money supply that propelled the shares had begun to spread beyond trading on rue Quincampoix. Property prices began to soar as the newly-wealthy owners of Mississippi Company shares traded them for luxurious homes in the city, as well as large estates in the countryside. Money also began flowing out into the broader economy, as shareholders sold shares, or borrowed against their value, to spend lavishly.

As prices began to rise for everything from land to wheat to fine imports from the Spanish Netherlands in late 1719, it marked a pivotal moment for the citizens of France: the arrival of inflation. It also marked the end of the Mississippi Bubble, and the beginning of the inflationary bust.

* * *

It has now been eighteen months since the Federal Reserve ended the massive quantitative easing program carried out in response to the Covid-19 pandemic, and given the long and variable lags with which changes in monetary policy affect prices, the early, first-order impact of that massive monetary expansion is only just now fading from the scene. The year-over-year change in the headline Consumer Price Index over the course of the past sixteen months reflects that: it has fallen from just below 9% to just above 3%, as commodity prices settled down after the dramatic increases in 2020 and 2021. The year-over-year rate of change in the core Consumer Price index, shown below, remains elevated over the range of the past 25 years, but has also fallen from its peak rate in 2022.

Yet there is far more to an inflation dynamic, once entrenched, than the early, first order reaction, as John Law eventually discovered. In late 1719, the first hint of trouble from beyond first-order reactions came when a small number of astute citizens no longer believed the proliferating notes of the Banque Royale were a trustworthy store of long-term value – and discretely sought an exit.

The closure of the Banque Royale on the last day of November 1719, along with the subsequent decrees which mandated use of its banknotes, were early signs that the market environment had pivoted away from the initial, exuberant expansion resulting from the massive growth of the money supply, and had begun to price in the full inflationary cost.

As prices soared for homes, land, and everyday goods, it shattered the underlying assumption that prices were mainly a function of supply, demand, and progress. People began to understand that prices could also change from an erosion in the value of the notes they held in their hand, and the closure of the Banque Royale in November 1719 resulted from a few of those people demanding to exchange their paper banknotes for something of trustworthy value – gold and silver coin.

The erosion of trust in the value of a currency is one of the main second-order impacts of large monetary expansions. Once that trust is lost, it is difficult, and sometimes impossible, to get back.

John Law found out in 1720 that restoring that trust ultimately involved sacrificing his entire scheme to bring prosperity to France, and relieve the Royal Treasury of its debts, by expanding the money supply. In the end, once the French citizenry lost faith that their banknotes would hold value, the stampede out of banknotes – and out of assets denominated in those banknotes – began. The prices of things which had previously only gone up – homes in Paris, land in the countryside, and especially Company of the West shares – suddenly found few bidders at any banknote-denominated price. The rush into gold and silver in 1720 ultimately restored the balance between the value of real assets and productive assets that had existed prior to 1719, and by 1721, rue Quincampoix was again a sleepy backstreet.

* * *

Since last year, the Federal Reserve has been attempting to achieve what John Law failed to do: restore faith in the value of the dollar before a second-order response— an entrenched inflationary psychology – takes root. Over the past year and a half, the Fed Funds rate has been taken vertical in that effort, increased from 0%-0.25% to 5.25%-5.5%.

The charts above place the rise in the Fed Funds rate over the past year and a half into perspective. This has been one of the largest increases in the Fed Funds rate in the post-war era; only the tightening campaigns in 1973-74 and the early 1980s witnessed sharper rate increases. As is shown in the bottom panel, on a percentage basis, i.e. scaled against the interest rate at the beginning of the rate hike campaign, the current cycle has produced the largest percentage increase ever.

At the same time as it has increased interest rates, the Federal Reserve has been doing what Law fatefully attempted to do at the Banque Royale in May 1720: shrink its balance sheet. After reaching its high-water mark at $8.965 trillion in April of last year, the Fed has disposed of $941 billion in assets, leaving its balance sheet at $8.024 trillion as of September 20th. This has had a predictable impact on the base money supply over the past year, highlighted below, and also in broader measures such as M2.

Early last year we reviewed the first and second time the Federal Reserve shrank its balance sheet, in the early 1920s and the mid-1930s. Those episodes highlighted an important point as the Federal Reserve embarked on quantitative tightening: there was little difference between the reaction of people and prices in 1720 versus the reactions of people and prices to early modern attempts to shrink the money supply. And over the past year, we have witnessed yet another demonstration of the impact of quantitative tightening, as stocks, bonds, commodities, and real estate have all felt the weight imparted by a shrinking money supply. Bank failures, like we saw earlier this year, have been a regular feature of broad declines in money supply historically.

Yet, at the same time, while consumer prices and asset prices have clearly felt the impact of the restrictive pivot in monetary policy over the past two years, the evidence has been growing that these first-order reactions may just be the initial response to a much larger secular pivot.

In his speech at this year’s annual conference of monetary policymakers in Jackson Hole, Wyoming, Fed Chair Jerome Powell highlighted this growing body of evidence that the economy is now being governed by a different set of inflationary forces.

He began by recounting a selective history of how inflation arose over the past few years, notably leaving out any mention of the increase in the money supply in the decade prior to 2020, or the massively expansionary policies of the Federal Reserve in 2020 and 2021. Instead, he framed the emergence of inflation as an almost happenstance meeting of pandemic and war:

The ongoing episode of high inflation initially emerged from a collision between very strong demand and pandemic-constrained supply. By the time the Federal Open Market Committee raised the policy rate in March 2022, it was clear that bringing down inflation would depend on both the unwinding of the unprecedented pandemic-related demand and supply distortions and on our tightening of monetary policy, which would slow the growth of aggregate demand, allowing supply time to catch up. While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.

On a 12-month basis, U.S. total, or “headline,” PCE (personal consumption expenditures) inflation peaked at 7 percent in June 2022 and declined to 3.3 percent as of July, following a trajectory roughly in line with global trends. The effects of Russia’s war against Ukraine have been a primary driver of the changes in headline inflation around the world since early 2022. Headline inflation is what households and businesses experience most directly, so this decline is very good news. But food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed…

On a 12-month basis, core PCE inflation peaked at 5.4 percent in February 2022 and declined gradually to 4.3 percent in July. The lower monthly readings for core inflation in June and July were welcome, but two months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal. We can’t yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters. Twelve-month core inflation is still elevated, and there is substantial further ground to cover to get back to price stability.

Powell concluded his speech with the following:

Turning to the outlook, although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role. Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.

Restrictive monetary policy has tightened financial conditions, supporting the expectation of below-trend growth… But we are attentive to signs that the economy may not be cooling as expected. So far this year, GDP (gross domestic product) growth has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust. In addition, after decelerating sharply over the past 18 months, the housing sector is showing signs of picking back up. Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy.

For those of us who have been following the Federal Reserve for a long time, the account above summarizing the sources of inflation represents a disingenuous characterization, at best. Lest we forget, the strong demand that collided with pandemic-constrained supply appeared just after the sharpest decline in GDP since the 1930s, and was the direct result of trillions of dollars of monetary and fiscal stimulus that followed. Without that stimulus, which was underwritten by the Federal Reserve, and which continued all the way into early 2022, there would have been no inflationary collision from such strong demand.

Selective histories like the narrative above exclude the primary reason inflation has proven stickier than expected over the last two years, and they also fatefully misdirect investors’ expectations. It is a misdirection similar to late 1719, when investors in Paris continued to wonder why the prices of homes, land, and goods of all kinds were rising all around them, while behind the scenes John Law continued to expand the supply of banknotes by leaps and bounds into 1720. Inflation of the kind we are experiencing today, like the inflation citizens of France experienced in 1719 and 1720, is the end result of a large increase in the base supply of money upon which all credit stands.

As is clear in the above chart showing the monetary base, the decline since 2021 is small relative to the growth since 2008. Based on this alone, it has not been difficult to understand why inflation has proven to be more persistent, and less transient, than expected.

It was also not difficult to understand the risk embedded in long-term bonds when Treasury yields were hovering at 1-2% in 2021 amid inflation that had climbed above 5%. Great Mistakes of this magnitude have a tendency to erode confidence once prices begin rising, and it is this type of second-order impact that we may be witnessing in the bond market right now.

The pivot shown in the chart above represents a secular pivot into a new regime, one that has simultaneously brought an end to the Bountiful Triple Dip investors have enjoyed over the past four decades, and an end to the Federal government’s ability to rely on artificially low rates to hide the cost of the growing national debt. It has set in motion a new dynamic that has been easy to miss amid the constant noise in the markets, but which is unmistakable when looked at through the lens of financial history.

Through that lens, the chart above represents an example of investors “seeking an exit,” similar to how astute investors in late 1719 sought an exit from paper livres once they lost confidence that the banknotes would hold their value in the long run.

One of the unmistakable signs of eroding confidence is a demand for higher yields, and this past month the yield of the 10-year Treasury note climbed to 4.6%, which is the highest it has been in sixteen years. With the Federal Reserve no longer buying them, the market yield for bonds has been unshackled from the largest player in the market, and the rapid rise over the past year reflects an emerging demand for more yield in exchange for holding Treasuries.

It also may reflect an early second-order erosion of faith in the long-term value of the dollar. This past month, the Federal debt climbed above $33 trillion for the first time, which is an increase of $3 trillion from $30 trillion just three months ago in June. The national debt, including its rising annual cost from rising interest rates, is now growing at a faster rate than the real economy. This is an unsustainable dynamic that is not dissimilar to the Mississippi Company’s need to continuously sell shares to fund its spending, all the while depending on the Banque Royale to facilitate the shares sales by issuing more banknotes. Long before the unsustainable nature of this relationship became obvious to the average French person as things fell apart, rates and real assets had begun to rise as astute investors made their exit.

Yet while the yield on long-term bonds has risen over the past two years, it is clear that the vast majority of investors in U.S. stocks and bonds have not yet headed for the exit. The underlying yield of a standard 60/40 portfolio of stocks and bonds sank to 1.78% below the yield cash receives when invested in short-term T-Bills, and the yield differential between a portfolio of stocks and bonds since 1920 with cash is shown below. If you are familiar with market history, every prior instance of a negative portfolio yield relative to cash over the past century – in 1929, 1970, 1973, 1980, 1989, 2000, and 2007 – has marked a major pre-recession market peak.

The negative yield above represents a looming issue for investors. Although a standard 60/40 portfolio suffered its largest loss in half a century last year, the ongoing faith in stocks and bonds, represented by the lower portfolio yield relative to cash, is a sign that investors largely believe Chair Jerome Powell that the Federal Reserve will maintain its restrictive monetary policy until the deed is done, and inflation returns to its 2% target. In this benign outcome, interest rates would decline back to the 2%-3% range, leaving stocks and bonds well supported at current valuations.

Yet if history is any guide, we are instead on the cusp of an erosion of the confidence in that benign outcome, which will see the yield from stocks and bonds move higher from where they are today.

The losses in stocks and bonds in 2022 represented an initial education of the impact rising yields higher inflation have on portfolio value, and for many those losses came as a shock. Yet with the combined yield of stocks and bonds far below the yield on cash, the bulk of the education from the ultra-low yields in recent years may still lie ahead.

* * *

Return to Memos, Articles, & Letters

The content of this document is provided as general information and is for educational purposes only. It is not intended to provide investment or other advice. This material is not to be construed as a recommendation or solicitation to buy or sell any security, financial product, instrument or to participate in any particular trading strategy. Not all securities, products or services described are available in all countries, and nothing herein constitutes an offer or solicitation of any securities, products or services in any jurisdiction where their offer or sale is not qualified or exempt from registration or otherwise legally permissible.

Although the material herein is based upon information considered reliable and up-to-date, Sitka Pacific Publishing, LLC does not assure that this material is accurate, current, or complete, and it should not be relied upon as such. Content in this document may not be copied, reproduced, republished, or posted, in whole or in part, without prior written consent from Sitka Pacific Publishing, LLC — which is usually gladly given, as long as its use includes clear and proper attribution. Contact us for more information.

© Sitka Pacific Publishing, LLC

Investment Management

Before investing, we will discuss your goals and risk tolerances with you to see if a separately managed account at Sitka Pacific would be a good fit. To contact us for a free consultation, visit Getting Started.

Macro Value Monitor

To read a selection of recent client letters and be alerted when new letters are posted to our public site, visit Recent Client Letters.